Abishek Raja Ram

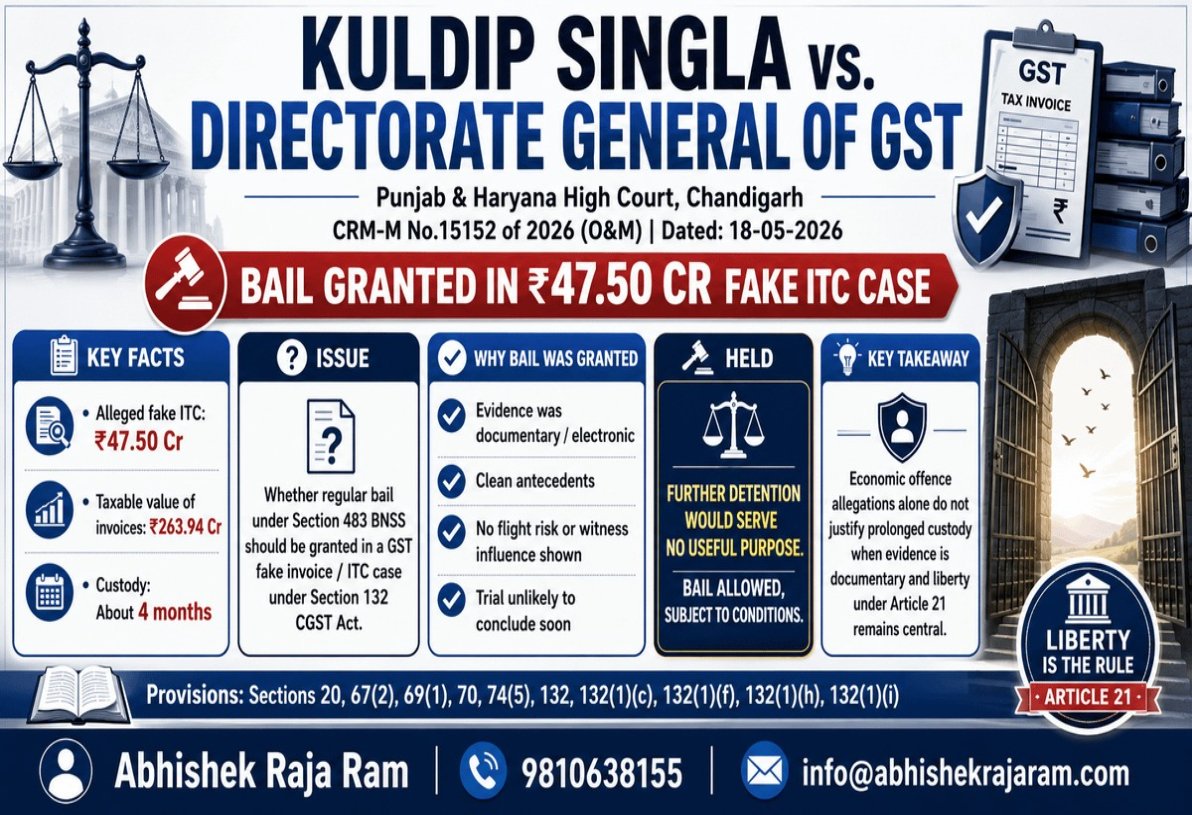

Assessee was in custody for about four months in an alleged ₹47.50 crore fake ITC case; Punjab & Haryana High Court granted bail as evidence was documentary, antecedents were clean and trial was unlikely to finish soon.

Issue:

Whether the Assessee, accused of fraudulent availment and utilisation of Input Tax Credit under Section 132 of the CGST Act involving alleged fake invoices of taxable value of ₹263.94 crore and ITC of ₹47.50 crore, was entitled to regular bail under Section 483 of the Bharatiya Nagarik Suraksha Sanhita, 2023.

Rule:

Bail is the general rule and jail is an exception. In GST offences, where the maximum punishment is limited, the evidence is mainly documentary/electronic, the investigation is substantially complete, and there is no material showing flight risk, witness influence or evidence tampering, continued custody is not justified. Arrest under Section 69 must also be based on “reasons to believe” and not on mere suspicion.

Application:

The Assessee had been arrested after search proceedings dated 19.01.2026 and formal arrest on 20.01.2026. The Department alleged fraudulent ITC availment without actual supply of goods. The Assessee stated that his unit was a registered furnace business and relied upon GST invoices, e-way bills, balance sheet and electricity records to show genuine transactions. The Court noted that the Assessee had remained in custody for about four months, had clean antecedents, the material evidence was documentary in nature, and nothing was shown to suggest that he would flee, tamper with evidence or influence witnesses.

Conclusion:

The High Court held that further detention of the Assessee would serve no useful purpose. The bail petition was allowed and the Assessee was directed to be released on personal and surety bonds, subject to conditions that he would not influence witnesses, would disclose his address, and would not leave India without permission of the trial Court. Observations were confined only to bail and not to trial merits.

Impact Analysis:

This judgment reinforces that in GST arrest cases, economic offence allegations alone cannot justify prolonged custody when evidence is documentary and trial is likely to take time. It strengthens the principle that liberty under Article 21 remains central even in high-value ITC matters.

Title : KULDIP SINGLA vs. DIRECTORATE GENERAL OF GST

Court : THE HIGH COURT OF PUNJAB AND HARYANA AT CHANDIGARH

Citation : CRM-M No.15152 of 2026 (O&M)

Dated : 18-05-2026

Provision : Under Section 20, 67(2), 69(1), 70, 74(5), 132, 132(1)(c), 132(1)(i), 132(1)(f), 132(1)(h)

Comments

0 visibleNo approved comments yet. Submit one from the form and it will appear here after admin approval.